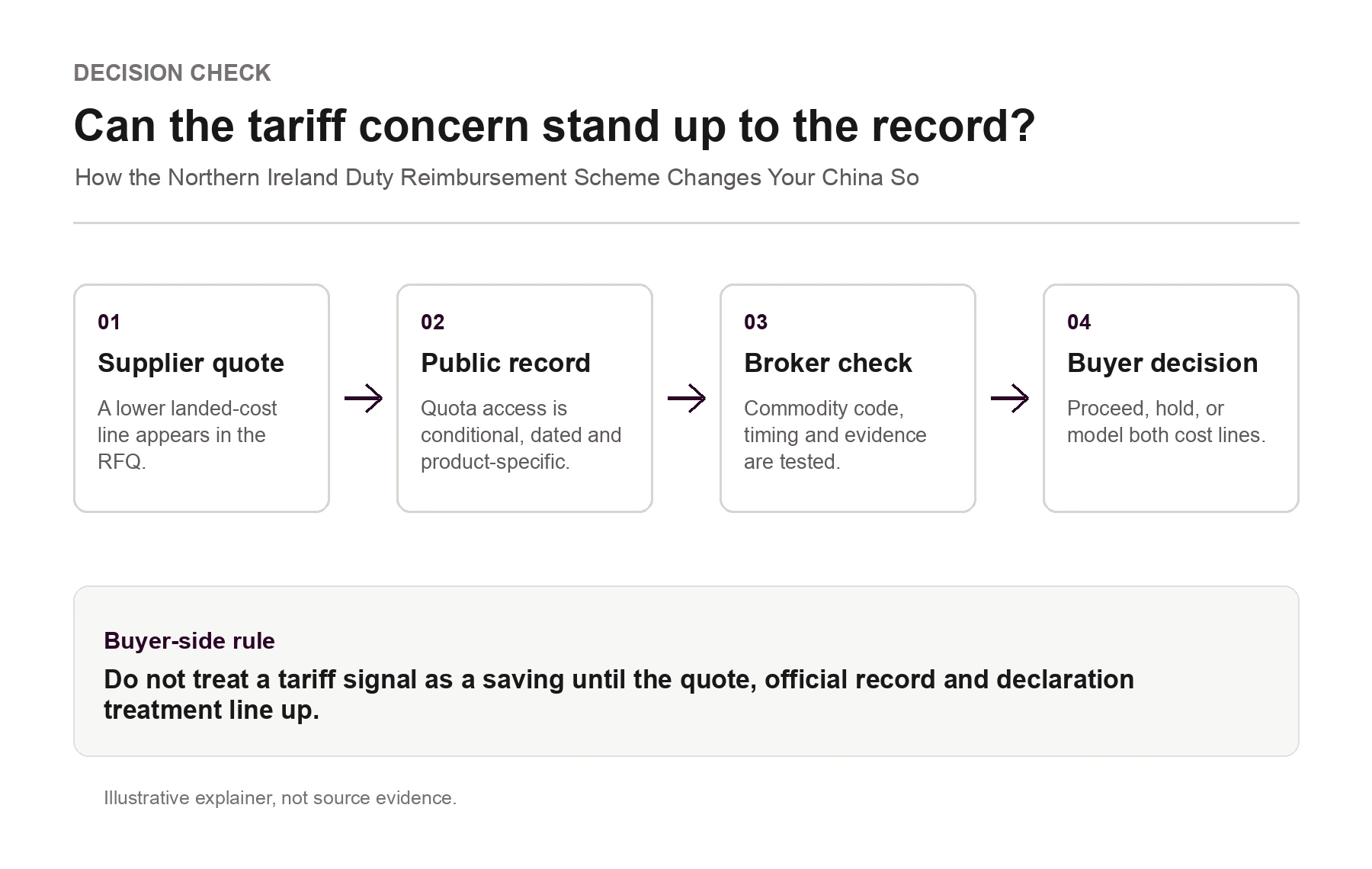

For China-origin goods moving into Northern Ireland, reimbursement is not only a claim deadline. It is an evidence trail: duty status, at-risk treatment, waiver use and broker records need to line up before the buyer relies on a cash-flow assumption.

Reader walks away knowing

- What the record shows about the June 2026 deadline

- Why this matters to UK buyers

- Buyer scenario: the commodity code assumption problem in RFQ comparisons

- Evidence Requirements: The Reimbursement Chain

What the record shows about the June 2026 deadline

HMRC guidance confirms that for duties paid between 1 January 2021 and 30 June 2023, you must submit your claim by 30 June 2026. For duties notified after 30 June 2023, you have three years from notification. State aid replenishment claims should be filed as soon as supporting evidence is ready—don't wait for your waiver allowance to be fully consumed.

This matters beyond the deadline itself. The existence of this scheme, and the precise evidence requirements HMRC enforces, tells you something important: the tariff line on your Northern Ireland goods is never settled at the purchase order. It can be contested, corrected, and—under the right conditions—reversed. That has direct implications for how you structure quotes, validate commodity codes, and build landed-cost models when sourcing from China.

Why this matters to UK buyers

The Windsor Framework governs how goods moving into Northern Ireland are treated. 'At risk' goods—those likely to move into the EU—attract EU import duties. The Duty Reimbursement Scheme exists because the UK government agreed that businesses shouldn't bear those EU duties permanently when goods ultimately stay in the UK market.

If you're sourcing industrial parts from a Chinese supplier and routing them through Northern Ireland to a UK customer or warehouse, the tariff treatment isn't binary. It depends on your commodity code declarations, your evidence that goods are not 'at risk' of entering the EU, and your ability to substantiate that position with documentation HMRC will accept.

The practical risk: If your supplier quotes a duty rate based on a commodity code assumption that HMRC later challenges—or if you claimed EU duty was not 'at risk' but cannot prove it—you may face a demand for duties already assumed off the table. The reimbursement scheme is the safety valve, but it requires evidence you may not have collected.

Buyer scenario: the commodity code assumption problem in RFQ comparisons

Here's where the scheme intersects with your sourcing decisions.

When you receive a quote from a Chinese supplier for delivery to Northern Ireland, the supplier's commercial invoice and packing list will include a commodity code. That code drives the EU duty rate. The supplier's quote may implicitly assume a certain duty treatment—waived, deferred, or paid and claimed back.

The scenario: You receive two quotes for similar industrial components. Supplier A uses one commodity-code position as the basis for the commercial invoice. Supplier B uses a nearby code for what appears to be the same functional part. The unit prices look comparable, but the landed-cost models can diverge once your broker confirms the actual duty exposure, 'not at risk' treatment and cash-flow timing of any reimbursement claim.

Without validating the commodity code with your customs broker before accepting either quote, you're not comparing like for like. The duty line in your landed cost model is only as reliable as the code underpinning it.

Evidence Requirements: The Reimbursement Chain

To make a successful claim under the Duty Reimbursement Scheme, you need to demonstrate:

- Goods identity: That the goods you've imported match the goods covered by your claim

- Tariff classification: That the commodity code used was accurate or has been corrected

- 'At risk' status: That you paid EU import duties on goods that were subsequently confirmed not to have entered the EU market

- Evidence of movement: Documentation showing goods remained within the UK market or were destroyed in NI

This is where many buyers discover gaps. If your Chinese supplier's shipping documentation, your customs entries, and your internal records don't form a coherent chain, HMRC will not accept a claim. The scheme doesn't just refund duties—it validates the evidence trail behind them.

Control points before the next commitment

Before you accept a new quote or place a deposit with a Chinese supplier for Northern Ireland delivery:

- Validate the commodity code with your customs broker. Ask them to run the code against the current UK Trade Tariff and confirm the applicable EU duty rate and any special conditions for 'not at risk' treatment.

- Audit your existing import records. For goods brought into Northern Ireland since January 2021, check whether EU import duties were paid and whether the 'at risk' determination is documented. If duties were paid on goods that stayed in the UK market, assess whether a reimbursement claim is viable.

- Update your landed-cost model with the reimbursement assumption. If you're claiming duties back under this scheme, the effective duty cost is time-dependent—it drops when the reimbursement is approved. Model the cash-flow difference, not just the headline rate.

- Request evidence-ready documentation from your supplier. Before shipment, ask for commercial invoices, packing lists, and certificates of origin formatted to support your 'not at risk' claim. A supplier that cannot provide traceable documentation is a liability, not just an inconvenience.

- Flag the June 2026 deadline internally. If you have unreconciled duty payments from the 2021-2023 window, your finance team needs to know. Claims submitted after the deadline will not be accepted.

The Duty Reimbursement Scheme exists because the post-Brexit Northern Ireland trade architecture is complex. That complexity doesn't disappear—it shifts to the evidence layer. The buyers who manage it well treat tariff assumptions as hypotheses to be verified, not facts to be accepted.

Plinth&Co's role is to keep the buyer's decision traceable: supplier-side checks in China confirm the material record, quote terms and shipment timing before the buyer commits.

Sources

Apply to claim a repayment or remission of import duty, or reclaim state aid used on 'at risk' goods brought into Northern Ireland – HMRC: https://www.gov.uk/guidance/apply-to-claim-a-repayment-or-remission-of-import-duty-on-at-risk-goods-brought-into-northern-ireland

Claim a waiver for duty on goods that you bring to Northern Ireland from Great Britain or countries outside the UK and EU – HMRC: https://www.gov.uk/guidance/claim-a-waiver-for-duty-on-goods-that-you-bring-to-northern-ireland-from-great-britain

CDSSG08040: Commodity Codes and Measurement Units – HMRC Customs Declaration Service guidance: https://www.gov.uk/hmrc-internal-manuals/customs-cds-volume-3-tariff-step-by-step-guide/cdssg08040

Control points before commitment

- Validate the commodity code with your customs broker. Ask them to run the code against the current UK Trade Tariff and confirm the applicable EU duty rate and any special conditions for 'not at risk' treatment.

- Audit your existing import records. For goods brought into Northern Ireland since January 2021, check whether EU import duties were paid and whether the 'at risk' determination is documented. If duties were paid on goods that stayed in the UK market, assess whether a reimbursement claim is viable.

- Update your landed-cost model with the reimbursement assumption. If you're claiming duties back under this scheme, the effective duty cost is time-dependent—it drops when the reimbursement is approved. Model the cash-flow difference, not just the headline rate.

- Request evidence-ready documentation from your supplier. Before shipment, ask for commercial invoices, packing lists, and certificates of origin formatted to support your 'not at risk' claim. A supplier that cannot provide traceable documentation is a liability, not just an inconvenience.

- Flag the June 2026 deadline internally. If you have unreconciled duty payments from the 2021-2023 window, your finance team needs to know. Claims submitted after the deadline will not be accepted.

Buyer-side control

Treat this briefing as a decision check before the next RFQ, deposit, shipment release or customs instruction. Confirm the live source record before using it as commercial advice. This is a buyer-side planning note, not legal, tax, customs or carbon-accounting advice; confirm final treatment with appointed providers or qualified specialists before acting. This is not legal advice, not tax advice, not customs advice and not carbon-accounting advice. Plinth&Co is not a factory. Plinth&Co is not a customs broker. Plinth&Co is not a tax adviser. Plinth&Co is not a law firm. Plinth&Co is not a carbon-accounting adviser.

Request a sourcing review