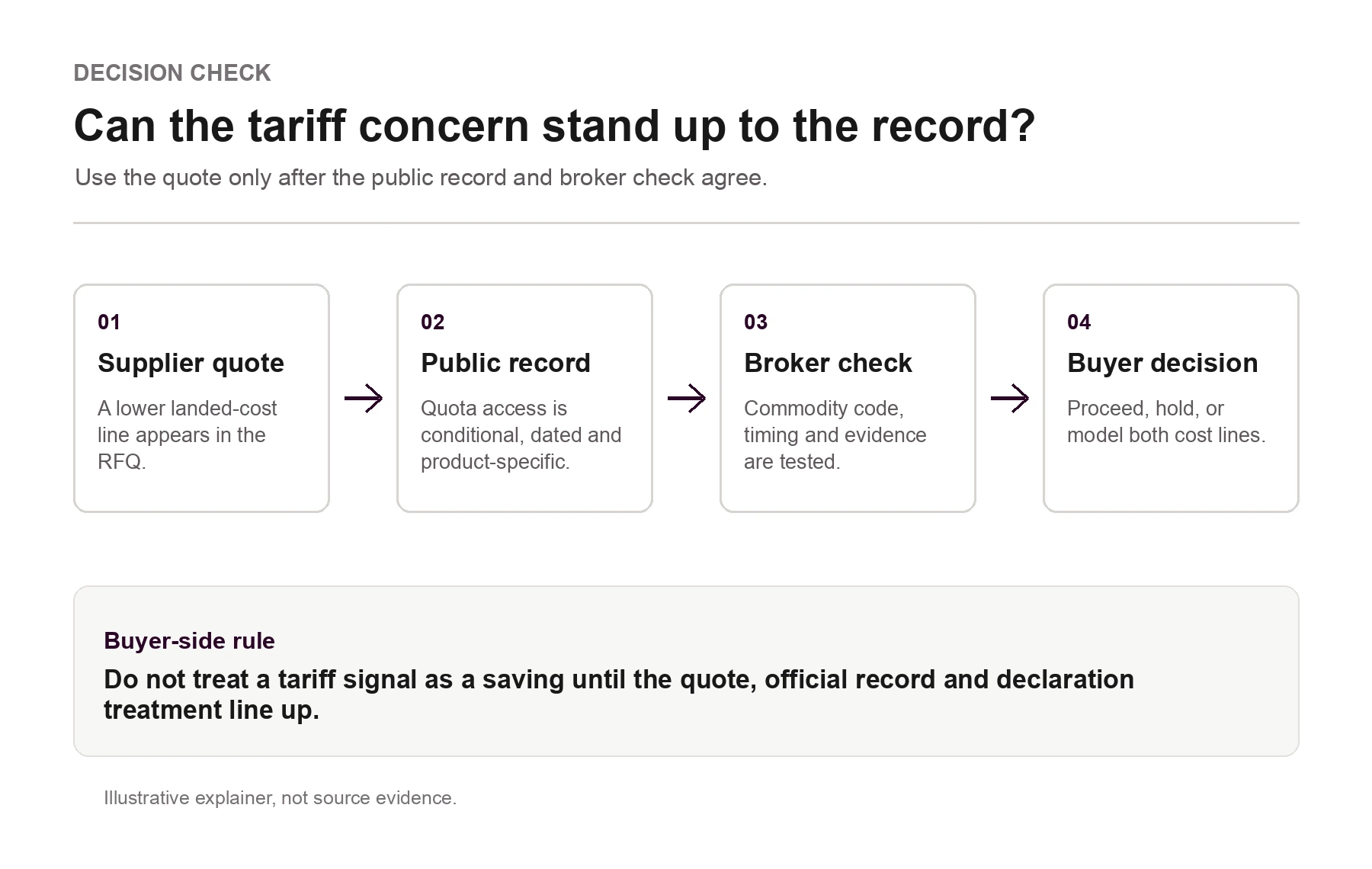

The useful question is not whether people are worried about tariffs. The useful question is whether the official record changes a UK buyer's live RFQ, quote comparison or shipment decision.

HMRC and HM Treasury have updated the reference documents for The Customs (Tariff Quotas) (EU Exit) Regulations 2020. The GOV.UK page lists a Tariff Quotas reference document, version 4.5, dated 12 May 2026, with entry into force on 21 June 2026.

For a UK buyer sourcing non-standard industrial goods from China, this is a check point, not a headline. A tariff-rate quota can affect the duty line only if the goods, commodity code, quota terms, date and evidence all line up.

Reader walks away knowing

- The record says quota access is conditional

- The supplier quote is not the customs decision

- A cheaper quote can be the weaker decision

- The landed-cost model needs two lines until evidence closes the gap

The record says quota access is conditional

The GOV.UK publication says the tariff quota documents detail product-specific tariff-rate quotas, including individual product volumes and rates, and the list of eligible goods and their authorised uses. It also says the statutory instrument establishes tariff-rate quotas for certain goods imported into the UK and a regime for managing most of those quotas using a first-come, first-served allocation system.

That matters because a quote can look cheaper when the spreadsheet assumes quota access. The official record does not mean every shipment gets the lower treatment. It means the buyer has to test whether the shipment can actually use it.

The buyer-side distinction is important. A public reference document can tell a buyer that a quota exists, what goods may be eligible and when a version of the document enters force. It does not, by itself, prove that a live shipment has the right classification, the right timing, the right evidence file or the right broker treatment.

The supplier quote is not the customs decision

Tariff quota assumptions sit in the same place as other landed-cost assumptions: behind the supplier's clean unit price. They can affect the comparison between two Chinese suppliers, the timing of a purchase order, the broker instructions and the import VAT cash-flow model.

The practical risk is not only a wrong percentage. It is a quote decision built on a duty line that was never checked against the product description, quota condition or expected declaration date.

If the buyer is working from an old internal spreadsheet, a supplier-provided landed-cost note or a previous broker answer, the quota line should be treated as provisional until it is checked again.

That is where sourcing and customs work often separate too early. The supplier may be able to describe the product and price it. The broker may be able to advise on the declaration. The finance team may be able to model duty and VAT. But the commercial decision is made before all three views have been joined into one usable order file.

A cheaper quote can be the weaker decision

A UK buyer compares two Chinese suppliers for a fabricated industrial component. Supplier A appears cheaper because the landed-cost model assumes a tariff quota applies. Supplier B appears more expensive because the model uses the normal duty treatment until the broker checks the commodity code and quota position.

The weak decision is to award the order to Supplier A because the first spreadsheet total is lower. The controlled decision is to separate the supplier price from the customs treatment, then ask what evidence supports the quota assumption.

The buyer does not need to become a customs adviser. The buyer does need a decision file that records the commodity code basis, the goods description, the source document date, the broker confirmation and the open assumptions.

The same file should also show what happens if the quota treatment is unavailable by the declaration date. Without that second line, the buyer is not comparing suppliers. The buyer is comparing one confirmed price with one unconfirmed customs assumption.

The landed-cost model needs two lines until evidence closes the gap

Use the quota question as a control gate:

Quota decision lineConfirmed landed cost = supplier price + freight + duty treatment + VAT cash-flow exposure + delay riskQuota delta = landed cost with confirmed quota treatment - landed cost with ordinary treatmentIf the quota treatment is not confirmed, the model should show both lines. That prevents a buyer from mistaking an unverified customs assumption for a supplier saving.

The second line is not pessimism. It is decision hygiene. It lets the buyer approve a supplier, pause the award, ask for more technical detail or instruct the broker without pretending the lower duty outcome is already secured.

The evidence request should go to both sides of the order

Ask the broker or customs adviser to confirm the commodity-code basis, whether the goods fall inside the quota description, whether the quota is available for the expected declaration timing, and which documents the importer should hold.

Ask the supplier for the facts that support classification: material, dimensions, function, process, drawing revision, invoice description, packing detail and any technical datasheet. Do not ask the supplier to "confirm UK duty" as if that alone closes the file.

The useful RFQ pack therefore needs supplier-facing and UK-facing lines. Supplier-facing lines make the goods clear enough to quote, manufacture and evidence. UK-facing lines make the import treatment clear enough to declare, value and reconcile. A lower landed-cost line is only usable when those two sides can be read together.

Control points before the next purchase commitment

- Mark every open quote that uses a tariff quota assumption.

- Split supplier price from customs treatment in the landed-cost model.

- Check the commodity code against the UK Trade Tariff.

- Record the GOV.UK source date used for the quota review.

- Ask the supplier for the product facts that support classification.

- Ask the broker or customs adviser what evidence the importer should retain.

- Keep the order decision pending until the lower duty line is confirmed or labelled as an assumption.

For Plinth&Co, this is a practical bridge task. The UK buyer owns the commercial decision. China-side execution work makes the supplier evidence, RFQ description and import file consistent enough for that decision to be made without hiding the risk in a spreadsheet.

Sources

HMRC and HM Treasury, Reference Documents for The Customs (Tariff Quotas) (EU Exit) Regulations 2020: https://www.gov.uk/government/publications/reference-documents-for-the-customs-tariff-quotas-eu-exit-regulations-2020 (live replay: HTTP 200; accessed 2026-05-24).

GOV.UK, Trade Tariff: look up commodity codes, duty and VAT rates: https://www.trade-tariff.service.gov.uk/find_commodity (used as the buyer-side commodity-code check point; accessed 2026-05-24).

HMRC, How to value your imports for customs duty and trade statistics: https://www.gov.uk/guidance/how-to-value-your-imports-for-customs-duty-and-trade-statistics (used for the landed-cost valuation control point; accessed 2026-05-24).

Control points before commitment

- Mark every open quote that uses a tariff quota assumption.

- Split supplier price from customs treatment in the landed-cost model.

- Check the commodity code against the UK Trade Tariff.

- Record the GOV.UK source date used for the quota review.

- Ask the supplier for the product facts that support classification.

Buyer-side control

Treat this briefing as a decision check before the next RFQ, deposit, shipment release or customs instruction. Confirm the live source record before using it as commercial advice. This is a buyer-side planning note, not legal, tax, customs or carbon-accounting advice; confirm final treatment with appointed providers or qualified specialists before acting. This is not legal advice, not tax advice, not customs advice and not carbon-accounting advice. Plinth&Co is not a factory. Plinth&Co is not a customs broker. Plinth&Co is not a tax adviser. Plinth&Co is not a law firm. Plinth&Co is not a carbon-accounting adviser.

Request a sourcing review